Every quarter our team analyzes the projects we work on with our 500+ PE firm clients to get a birdseye view of the market. We recently compiled our Q3 findings into our Q3 2022 BluWave Insights Report. Request your copy.

Key findings from Q3 ’22 include:

Value creation activity has increased 11% YoY.

Human capital remains PE’s primary area of focus at 36% of all Q3 activity.

BluWave serves a trusted role with more than 500 of the world’s leading private equity firms and thousands of proactive businesses by connecting them with the best-in-class third parties to help build value with speed and certainty. From our unique vantage in the private equity landscape, we’re able to glean insights into how and why the best business builders in the world are assessing opportunities and building value in their portfolio companies. Here are some of the top takeaways from the BluWave Activity Index during Q3 2022.

First and foremost, value creation remains key in private equity. Despite the unsteady economic landscape, PE firms are equipping their portfolio companies with resources to maintain the momentum of previous value creation efforts. The BluWave Value Creation Index shows a more than 11% increase in Q3 value creation activity year over year. It is evident that PE firms are running towards the storm, treating economic uncertainty as an opportunity rather than a setback.

Number two, technology is surging as digitization continues to be embedded in the post-COVID world. Private equity firms are equipping portfolio companies with data and analytics capabilities to enable data-driven decision making and workflow automation. We’ve seen technology activity rise from 8% of all activity in Q3 2021 to 15% of all PE activity in this past quarter, and we expect to see technology activity remain high as firms continue to invest in subscription-based software companies due to their stability during volatile economic times.

Lastly, human capital remains private equity’s primary area of focus accounting for 36% of all activity in the BluWave Activity Index for Q3 2022. Firms continue to take strides to ensure the teams in their portfolios are top notch and well-equipped for success. This quarter we saw a surge of PE firms bringing in “wartime generals” with specialized skillsets equipped for the “new now” that can help guide portfolio companies to success in the current economic environment.

It is our hope that the information in the Q3 BluWave Insights Report will give you incremental edge as you build the best businesses in the world. If you’d like to learn more and get the report, please contact any member of the BluWave team or follow the link below. Onward.

BluWave works with over 500 PE firms from around the globe as well as their portfolio companies and proactive independent companies, connecting them with BluWave-vetted, best-in-class, third-party service providers across a variety of resource and functional areas. From information technology and manufacturing to healthcare, consumer goods, and beyond, our clients are expert business builders. In other words, they have their heads in the game and their hands on the pulse of news and insights you can use.

Check out the latest, curated collection of our clients’ musings on turning current market conditions and macroeconomic challenges into opportunity, human capital due diligence, and more.

Blackstone’s Senior Managing Director and Chief Investment Strategist shares an evaluation of recession indicators while considering near-term macroeconomic challenges. His sentiment is that even though a recession looks like risk at the forefront, recessions are cyclical and business leaders who understand this have an advantage in the long run. Zidle digs into current market conditions and historical examples of different recession outcomes.

ParkerGale Operating Team Partner, Jimmy Holloran, is joined by Laura Queen, founder, and CEO of 29Bison, a human capital consultancy focused on the PE space. They discuss how talent investments can unlock organizational true value and break down the human capital due diligence basics – what it is, how it’s done, and why it’s the fastest-growing of all the diligence workstreams.

Veridapt CEO David Thambiratnam and Chief Technology Officer and Co-Founder Sean Birrell join the 2022 Macquarie Technology Summit to discuss the role of hardware and software technology in monitoring commodities while battling ongoing supply chain challenges, managing risks, and optimizing operations.

Insight Partners Managing Director Praveen Akkiraju dives into how business builders can invest and prioritize human capital not only to survive the bad times, but to also be focused and ready to accelerate once the good times arrive. He shares why resilience plans start with protecting your human capital.

KKR Partner and Co-Head of European Private Equity Philipp Freise outlines how the major geopolitical shifts will fuel the European economy, the beginning stages of untapped digitization opportunities, and how the private economy can remain resilient and embrace these challenging times, thus driving global transformation.

Here’s what some of our clients had to say last month on creating value with digital transformation, boosting operating speeds, software delivery competence, and more.

Every quarter our team analyzes the projects we work on with our 500+ PE firm clients to get a birdseye view of the market. You can request your copy here to view all of the trends that we have seen over the past quarter.

Key findings from Q2 include value creation remaining strong due to the record number of deals made at robust valuation multiples during 2021, inflation continuing to wreak havoc on global economies, and the recessionary pressures availing substantial opportunities for all of the best business builders.

Learn more about the insights we gleaned from the report by watching the video below.

BluWave has a unique vantage in the North American economy. While working with more than 500 of the world’s top business builders, we’re able to understand unique insights into how and why the best business builders in the world are assessing opportunities and building value in their portfolio companies. Here are some of the unique insights we generated during Q2 2022. The name of the game in the second quarter was value creation. Value creation accounted for 68% of all activity funneled through the BluWave engine. Value creation was so robust during this last quarter for a number of reasons. Number one, private equity firms invested in a large number of companies last year so they’re acting on those investments to begin transformation. Number two, deal flow is down. A lot of the best companies were sold last year. Other companies are pausing their ambitions as the economic cycle is softening and the results slow in kind. The other mega trend that is readily apparent in our data is the specter of inflation. The private equity industry is not resting on its laurels. It’s taking aggressive action to raise prices, reduce costs, and bring in the right people with the right skills for the current times. It’s our hope that the data and insights we’re sharing will help you build your business with more speed and certainty. If you’d like to learn more and get the full report, please contact any member of the BluWave team or follow a link below.

It was refreshing to be back in person with hundreds of PE ops partners to learn from their first-hand perspectives. Key takeaways included:

Executing value creation means that human capital remains a top priority for PE firms.

Ensuring the right management team and board leadership are in place allows for efficient execution against the value creation plan. Resource scarcity has had an immense impact on firms’ abilities to implement and execute plans. Industry leaders discussed tips for how PE firms can source and retain the right people at our recent human capital forum.

Leveraging technology to increase efficiencies is non-negotiable.

The aforementioned human capital challenges have tremendously accelerated digital transformation plans. PE firms are laser-focused on leveraging technology to increase efficiencies and reduce manual tasks to align with value creation plans. This allows portcos to reallocate resources to higher impact areas and rely on technology to solve for the monotonous, repeatable workflow.

Building trust with portcos’ management teams early on is essential.

Trusted partnerships between PE firms and their portfolio companies are vital to a successful investment. Building executive buy-in earlier on in the diligence process with a people-centric approach puts PE firms in a win-win situation. When the (right) management team has ownership in the decision-making process, this creates invaluable efficiencies between the PE firm and portco leadership teams.

If you’re interested in learning more about any of these, contact us here. You can also check out some of these resources:

We recently spoke with Mark DeBlois and Rufus Clark, two of the Co-Founders and Managing Partners of Bunker Hill Capital, a private equity firm investing in entrepreneur and founder-owned lower middle market companies in North America. Bunker Hill has offices in Boston, MA and San Diego, CA.

The four partners at Bunker Hill have worked together for over 20 years as private equity investors with lower middle market companies. As lead investors, they actively work with portfolio companies leveraging their extensive board-level and strategic planning experience.

When I caught up with them on the journey of Bunker Hill Capital, it was refreshing to hear how, in a world consumed with change, nothing can quite replace years of dedicated experience, a focus on relationships, and a time-tested investment ethos.

Tell us about the founding of Bunker Hill Capital.

We were senior members of the buyout team at BancBoston Capital, one of the largest bank-affiliated investment companies in the US, and it became increasingly apparent that going it alone would allow us to control our own destiny. Having a private equity mindset is different from how a commercial bank approaches investing, and we wanted to manage the business without these inherent limitations. Also, being able to change our investment strategy and how we invested was just as important.

An example is our ability to work closely with a variety of value-added partners including operating professionals and strategy consultants. Our relationships with them are a cornerstone of how we invest, proactively create value, and build relationships across the marketplace. As part of establishing Bunker Hill Capital, we were able to develop relationships with a wide range of strategic partners that was not possible when part of a large institution.

So, we spun out to start our own firm, Bunker Hill Capital, just under two decades ago.

Since then, how has the market changed?

The transaction dynamics have changed with the growth in the alternative asset class. The amount of capital flowing into the asset class has increased dramatically as has the number of PE funds, pushing up multiples over time.

Our core market, the lower middle market, includes companies with revenues between $5 million and $100 million—of which there are approximately 360,000 in the United States today. Compare that to the next level up, where there are about 22,000 companies with revenue between $100 million and $500 million, so our opportunity pool is 16 times larger.

In our market, we can source deals either as one-off deals directly from owner-entrepreneurs as sellers, through intermediaries such as accountants and attorneys, or through limited auctions, where an investment bank brings together people they know who can close deals and who have years of experience in the lower middle market, such as ourselves.

So, it’s actually the market dynamics in this end of the lower middle market that have not changed as dramatically that allow us to continue to reap the benefits.

An area where we have seen change is increasing prices in each market segment. However, as much as they have all gone up, the relative delta between the lower and upper middle markets has remained constant. For example, hypothetically as the first PE owner we may pay between 6.5x and 7x on EBITDA for the companies we invest in (compared to 2003, which was 5-6x). We then sell these companies to strategic buyers or the next market level up—large PE funds that pay between 8x to 10x on EBITDA multiples. So when we sell our companies to these strategic buyers, we capitalize on this multiple arbitrage.

What differentiates Bunker Hill Capital?

Bunker Hill Capital is well-known in the lower middle market, having been in this market segment for over 20 years, which is very unusual.

We are unique in that we have the luxury of staying in the smaller end of the market. People tend to think bigger is better. We think we can have more impact strategically on these smaller companies over a shorter period of time, compared with the larger deals that are more like steamships: huge and take a lot longer to turn.

Our key criteria for buying companies is to be the first PE owner buying from founders and owner-entrepreneurs who either want to remain in the business or have identified their management team. This is 70 to 80 percent of our deals.

This is important because these founders are looking to crystalize the value of their sweat equity, and take some of their chips off the table for a variety of reasons. Finding a partner who will risk their own money to do this and take the company to the next level is key. The founder can then continue to enjoy the benefit of their minority capital stake, thereby continuing to increase their wealth by getting a “second bite of the apple.”

We do extensive strategy and infrastructure work at the companies we buy to allow them to scale. The larger funds, in the next level up, buy from folks like us as they can’t grow just organically; they need to grow through acquisition to get the kind of returns and exit multiples to satisfy their investors. Therefore, by definition, they must combine organic growth with acquisitions. And that’s where we come in.

How is Bunker Hill approaching the investment process to generate differentiated returns?

Early on from Fund I we refined our due diligence process, such as building relationships with our network of strategic partners. A lot of these refinements we did during Fund I, so the due diligence process we have now follows the same repeatable model. This has resulted in a time-tested methodology.

We believe the 20+ year evolution of our methodical investment process is world-class. Being a fiduciary to our limited partners, we are very hands-on in the businesses we invest in. We collaborate closely with our management teams and give them the tools they’ve never had before to better serve the business.

Post-close, we go through a 90- to 120-day strategic planning process to implement the findings from our detailed pre-sale due diligence and formalize the strategy into what we call a “Full Potential Roadmap.” This is coupled with a “Key Initiative Tracker,” which breaks down the Roadmap into an implementable plan, and is then tracked and monitored weekly and/or monthly with clear accountability and performance-based outcomes.

Finally, this plan is driven by the growth initiatives we are going after and how we want to scale the business’ revenue. But perhaps more rewarding is that after going through the process, most of the CEOs thank us for these invaluable tools that help them empower their own people, hold them accountable, and transform their business.

How is working with a Founder-Owned business unique?

Owner-entrepreneurs and founders can run the spectrum on experience and/or business sophistication, so identifying where along this spectrum the founder is and recognizing this is part of our due diligence process.

We place enormous emphasis on these founder relationships and if the chemistry is not quite right, we may decide not to proceed for the benefit of all parties. This is where the buck stops, especially if the owner is critical to the business.

Working with a wide variety of owners and CEOs is like working with any new person. We don’t delegate this relationship down to junior staff, as it is very personal at the managing partner level. You have to quickly figure out their strengths, growth opportunities, skills, and communication style, and we have to work with all of this while going through complex transactions – working through strategy, implementation, and everything else that goes along with the transaction.

Sometimes the owner is the CEO, and sometimes that’s not the case. The strongest CEOs are proactive and are on top of the Key Initiative Tracker. Some of the best CEOs we have worked with are self-aware enough to know where their highest value is in their role with the new company, including using the Key Initiative Tracker to mentor and track their direct reports, and then leading the charge on implementing these growth initiatives throughout the organization.

Can you talk about the role of ESG in Private Equity?:

ESG is a hot topic now. Most PE firms were doing a portion of this before it really got labeled. We were always doing environmental and social due diligence with potential investments.

Historically, we have intentionally looked at where the company could be more environmentally friendly and socially aware. Examples include increasing the recycling of waste materials, cutting down on energy consumption, and recruiting the most qualified candidates for roles.

Within our Key Initiative Tracker, we formalized this by putting in a group of ESG initiatives and being more explicit about it with our companies.

For example, we are being more proactive when we are sourcing overseas with a supplier code of conduct that includes detailed standards that our suppliers have to abide by.

On the social side, we have a strong bench of DEI candidates throughout our companies. DEI is built into our recruiting approach when hiring the most qualified person for the job.

For someone entering Private Equity in today’s landscape, what advice would you offer to them?

Find partners you can trust and work with. There are lots of ups and downs. You work hard and go through a lot— it can be very rewarding, but you need to have trusted partners over a long period of time.

You don’t know what you don’t know, and like everything else there is an evolution. There is no replacement for experience. It is complex enough doing what we do, and over the past couple of decades we have been able to cultivate relationships and refine our process along with the types of companies we invest in.

Also, don’t be afraid to surround yourself with smart people, not only inside the GP but also with your outside advisors. The relationships we have with our world-class executive network have been mutually beneficial. For example, our CEOs that are still assisting in our deals 20 years later is only something you can build over time. You can’t flip a switch and say, “I want that Day One.” It comes with being in the trenches together over a long period of time.

Interested in hearing what other PE experts have said in our interview series? Check them out here.

ACG InterGrowth 2022, known as the premier dealmaking conference, was conceptualized to build and strengthen relationships between private equity firms and investment banks. This annual conference allows PE industry leaders to gather and discuss key trends. Last week was filled with cybersecurity, DE&I, and supply chain thought leadership conversations, plus some Las Vegas style poolside networking.

As hundreds of private equity professionals and investment bankers filled the ARIA Resort & Casino from April 25-27, 2022, our team was able to re-connect with familiar faces as well as meet new ones.

“You could feel the eagerness to be back in person the moment you arrived. From founders to deal teams to business development professionals, the atmosphere was engulfed by ideation and excitement,” says Michael Mahan, BluWave Account Management Director.

Here are some of our team’s top takeaways from our largest conference back in person:

Quality Deal Flow Challenges

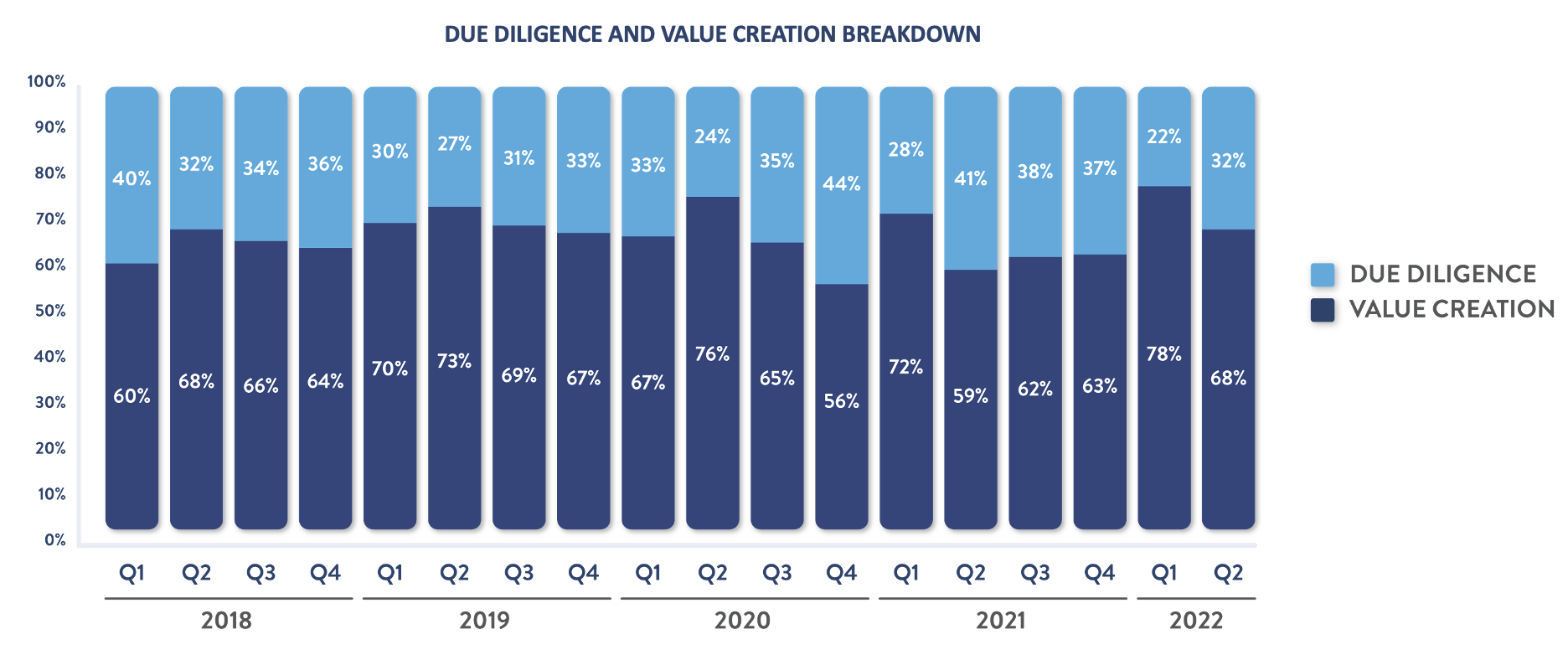

PE firms broadly shared that activity is slower compared to last year at this time. Our data confirms this as due diligence projects have declined YoY, from 28% of the BluWave Activity Index in Q1 2021 to now 22% in Q1 2022. While overall deal flows are beginning to increase, deal teams expressed that quality deals are hard to come by.

Lights, Deals, Action!

While ‘digital transformation’ remains a top buzzword, we know that top-performing, proactive PE firms and their portfolio companies are looking to transform their businesses, not just optimize them. Industries such as manufacturing and supply chain are dependent on new technologies to scale growth and meet the industry demand post-pandemic.

Market Differentiation

Building brand equity to differentiate your firm is important in today’s crowded landscape. With less quality deals in the market, it is mission critical for firms to remain top of mind with investment bankers. PE firms are finding creative ways to do this through utilizing specialized resources that can help them with their internal branding, & more.

ACG InterGrowth 2022 exceeded our expectations, and it was great to have the opportunity to connect with so many individuals in person. If you were unable to attend the conference, but are interested in connecting with us, contact us here.

BluWave Account Manager Morgan Murphy concludes, “This year’s conference was instrumental in continuing to build our relationships with PE firms face-to-face. Until next year!”

BluWave works with over 500 PE firms from around the globe as well as their portfolio companies and proactive independent companies, connecting them with pre-vetted, best-in-class, third-party service providers across a variety of resource and functional areas. From information technology and manufacturing to healthcare, consumer goods, and beyond, our clients are expert business builders. In other words, they have their heads in the game and their hands on the pulse of news and insights you can use.

Check out the latest, curated collection of our clients’ musings on everything from retail industry news to ESG and CEO perspectives.

Blackstone recently gathered CEOs across their portfolio companies for their annual CEO Conference. While we live in a world where it’s rare for anyone, nonetheless decision-makers, to agree on political or major topics as well as growth and business strategies, here are some key insights that brought the group together. Highlights include recruiting and retaining talent, finding success in simplicity, and keeping ESG at the top of their agendas.

Vice President at Baird Capital, Becca Schlagenhauf, dives into root causes of grid instability and how the growth in demand can lead to growth in distributed energy resources. The movement towards green energy still comes with its own sets of challenges associated with cost and reliability. As new technologies are being brought online, this has created solutions that are going to be vital to the global electricity infrastructure moving forward.

Learn about Heartwood Partners’ continual increased interest in different recycling and environmental services businesses and about their notion to “do well by doing good.” Their ultimate interests lie in the recyclability of finished products after they have been used by end-customers. Opportunistic themes and strategies involve packaging, agriculture, consumers, and more.

MiddleGround Capital Founding Partner, John Stewart, spills his secrets on how their operational focus enabled their companies to build resilience prior to and during the pandemic. Due to the pent-up demand from 2020 in manufacturing and industrials, Stewart highlights the opportunities for American workers as manufacturing wages are spiking. With the industry being under-invested as a whole for the past few decades, the opportunities for business to take advantage in technologies to produce more products is unmatched.