Connecting with a service provider you can trust is like looking for a great dentist. Once you find “the one,” you wouldn’t put your teeth in anyone else’s hands.

The same goes for your business. After a successful engagement with a trusted third party, you save a lot of time by contacting them directly the next time you have a need.

There are reasons you have go-to service providers: they’re fast, reliable and they know your business.

But if you love them so much, you’re probably not their only client. Far from it.

So what happens when you reach out and they tell you they simply don’t have the capacity to take on more work on the timeline you need? Or worse yet, they give you their B-team.

There are a number of reasons service providers could suddenly be in high demand. A bounce-back from a recession. A surge in deal flow. A hot new trend of which everyone’s trying to stay ahead.

When this happens, BluWave is on standby with a deep bench of trusted, PE-grade third parties who can deliver the exceptional work you expect no matter what your industry.

In fact, we experienced this post-COVID recovery when the whole world got back to business at once and it seemed like there wasn’t enough help to go around. At that time, we heard from dozens of private equity firms that couldn’t book their preferred third-party resource.

We helped those firms by connecting them with industry-specific firms and consultants that understood their business’s most pressing needs.

Every service provider in the Business Builders’ Network has gone through a rigorous vetting process, giving us confidence in every match we make whether it’s a first-time engagement or a repeat relationship.

BluWave founder and CEO Sean Mooney has three tips for organizations when their usual service providers are at full capacity.

1) Use Alternatives

“If you’re go-to is sold out, don’t try to force them into giving you capacity. You’ll get the C team,” Mooney says. “There are plenty of other comparable PE-grade specialists that you should use.”

2) Use Substitutes

“There are other diligence and value creation products that go by a different name but still serve your need,” he adds. “For instance, if you can’t get a commercial due diligence group to meet your deadline, use a voice of the customer group to do a deep dive on your target’s customers.”

3) Use Independent Consultants

“There’s a select world of independents who spun out of name-brand shops and can give you the same product at a fraction of the cost,” Mooney says. “This cohort works well not only for commercial diligence, but also for operational and HR diligence as well as value creation.”

Mooney recognizes that trusting your most important work to new partners can be scary. With the right introduction, though, the risk can have a huge payoff.

“Using new groups can be nerve-racking,” he says, “but the BluWave network of PE-grade resources is on standby to meet your specific needs.”

Whether your go-to service providers are at full capacity, or you just don’t know who to turn to, give our research and operations team a call. They’ll connect you with a shortlist of exact-fit third parties within a single business day, and be by your side until the completion of the project.

Service Provider Type: Specialized Interim Executives

Industry: Industrial Distribution and Services

The Need

Interim CFO, COO Team for Turnaround

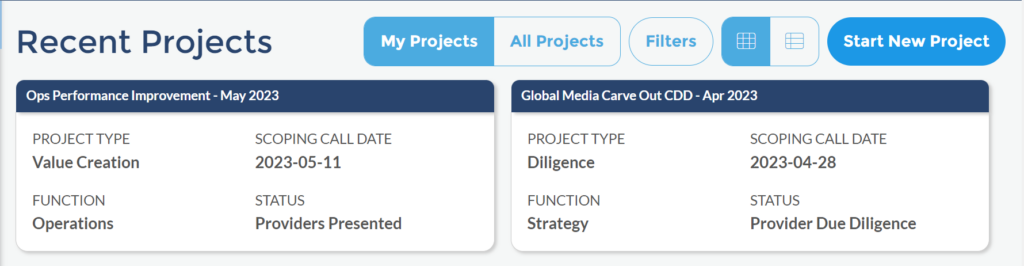

A multi-generation family-owned business faced significant challenges due to declining financial performance and market dynamics. The company also suffered a cyberattack that exposed weaknesses in its IT infrastructure. Recognizing the need for help, ownership sought external expertise to guide them through a comprehensive turnaround.

The Challenge

Revitalizing Profitability, Building Value Creation Foundation

The business grappled with challenges related to its profitability and internal capacity. The cyberattack highlighted the urgency of implementing an effective IT infrastructure and strengthening the leadership team. An outside advisory board, hired by the family, immediately recommended that a multifunctional team with interim CFO and COO turnaround skills was crucial. The objective was to streamline operations, reduce costs and create a sustainable foundation for renewed growth in order to rebuild value for the family and company stakeholders. Trusted advisors introduced the family to BluWave.

How BluWave Helped

Proven Executive Duo a Perfect Match

BluWave sprung into action, first taking time to understand the unique situation and the factors needed for success. BluWave then swiftly matched the family business with a highly experienced interim CFO and COO duo from the BluWave Network who understood the complexities of the company’s industrial markets and possessed a background in turnaround and operational performance improvement. Because of the ready-to-go nature of the PE-grade, pre-vetted Business Builders’ Network, BluWave was able to introduce the perfect fit executives to the company’s family ownership within a single business day.

The Result

Accelerated Profitability, High-Valuation Sale

The transformative efforts led by the interim CFO and COO turnaround team resulted in significant improvements in profitability and operational efficiency. The company quickly took action to stabilize and reinvigorate revenue and optimize human capital, which increased EBITDA from approximately breakeven to more than $10 million in less than 18 months. The cultural shift toward performance and accountability empowered the employee base, enabling them to rise to the challenge and drive positive change throughout the organization. The family was then sold the business to a top private equity firm at a nine-figure valuation.

The collaborative partnership between the family, the interim CFO and COO combo and BluWave facilitated a comprehensive turnaround, leading to increased profitability, operational efficiency and a transformed organizational culture. The company continues to thrive under new leadership, supported by the foundation laid during the turnaround engagement. In fact, the current full-time CFO and the former turnaround interim CFO connected by BluWave keep in touch to this day.

There had to be a tremendous amount of change within the leadership team because we were driving a culture of change toward performance and profitability. They were invigorated by the accountability they saw and the opportunity, and they rose to that challenge.

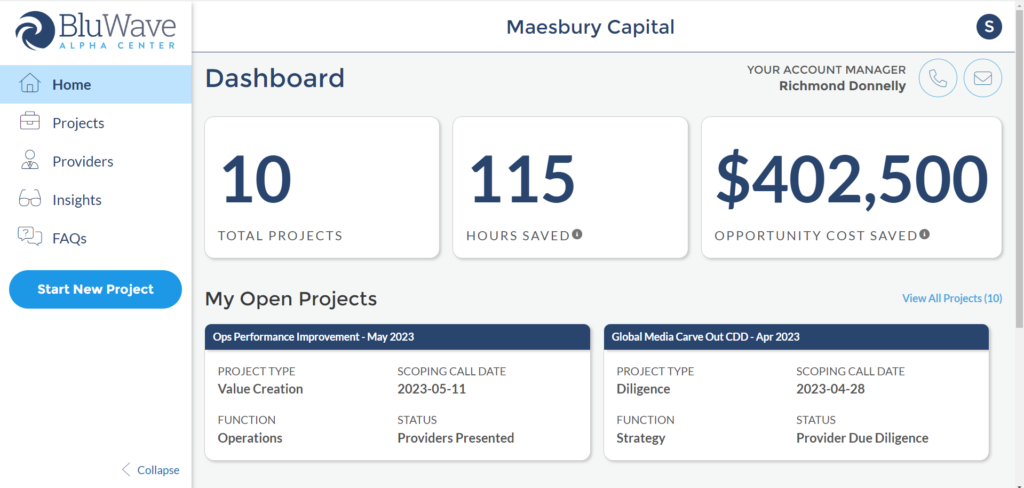

At BluWave, we understand the challenges that proactive business leaders face in finding and engaging with top-tier service providers. That’s why we’re excited to introduce the BluWave Alpha Center, a cutting-edge portal designed to streamline your third-party sourcing, project management and data insights processes.

This AI-driven platform empowers private equity firms, portfolio companies, and private and public businesses to stay ahead of the curve and be at the forefront of modern value creation.

“We are excited to introduce the BluWave Alpha Center, a game-changing platform that empowers private equity firms to accelerate their business-building efforts,” said Sean Mooney, a former PE deal partner and BluWave’s founder and CEO.

Collaborating effectively across teams is crucial in today’s fast-paced business landscape. With the BluWave Alpha Center, you can ensure that your entire team is on the same page. Our platform provides a centralized hub for insights, intelligence and white-glove service, facilitating seamless teamwork. From tracking evaluation processes to scheduling meetings, the Alpha Center simplifies collaboration, ensuring that everyone is working toward a common goal.

Accelerate Your Project Kickoff

In the private equity industry, time is of the essence. The Alpha Center enables you to kick off searches to get connected with the exact PE-grade third parties you require at the exact time you need them. By accessing your Alpha Center account, you can submit high-level criteria to our Research & Operations team and schedule scoping calls with ease. Our best-in-class third-party resources are just a few clicks away, allowing you to accelerate your project kickoff and make progress at the speed of private equity.

Efficient Project Management Made Easy

Managing projects efficiently is key to achieving success. The Alpha Center provides powerful project management tools that simplify the process and enable you to make informed decisions faster. Evaluate service providers, manage onboarding processes and track progress from initial review to contract signings all within a single platform.

This streamlines your project management, saves time and ensures that your deal processes stay on track, aligning with your key objectives and improving outcomes.

Data management is often a challenge, with valuable information scattered across different platforms. The Alpha Center acts as a comprehensive repository, bringing together all your project insights into one place. Catalog projects undertaken through BluWave, access information on providers and capture feedback on past performance.

This centralized tool ensures that you can easily search and share valuable insights across your organization, reconnect with previously vetted resources and facilitate informed decision-making.

Real-Time Insights and Market Comparisons

Stay informed and benchmark your performance with real-time insights and market comparisons. The Alpha Center provides dynamic quarterly updates and detailed reports on project trends, the Value Creation Index and rising priorities in the industry.

Compare your personalized dashboard with these insights to ensure that you’re aligned with the market and leveraging the full potential of your third-party engagements.

The BluWave Alpha Center is more than just a platform – it’s a game-changer for private equity firms and businesses looking to optimize their business-building processes. With enhanced collaboration, accelerated project kickoff, efficient project management, centralized data management and real-time insights, the Alpha Center empowers you to make informed decisions, drive value and stay ahead of the competition.

“We’ve been working with a group of top PE firm beta users, taking their feedback and updating what will be a continually evolving resource,” BluWave Head of Technology & Insights Houston Slatton says. “We’re excited to support existing clients and welcome new ones to the next generation of BluWave.”

Discover the power of the BluWave Alpha Center by scheduling a demo today and unlock the full potential of your business-building strategies.

Why should a private equity firm or a private or public business hire an interim chief technology officer?

In today’s fast-paced digital landscape, technology leadership is crucial for businesses seeking to innovate, streamline operations and stay ahead of the competition. But finding the right CTO can be a challenge, particularly for private equity firms managing a portfolio of companies, or private and public companies undergoing significant change. This is why outside resources that are intimately connected to the top temporary tech executives can give you a huge advantage.

SIGN UP FOR OUR NEWSLETTER

Stay up to date with the latest PE trends, case studies on how we’re helping business builders win and more.

“For companies with tech products – internal or external – a good CTO can provide necessary leadership to make sure those products are built on time, at budget and with high quality,” says Houston Slatton, BluWave’s head of technology. “They can also play a role in architecture, validating the tech stack and helping determine the right path forward in growing organizations.

Interim CTOs can serve as a stopgap solution to either turn things around or simply keep the business moving forward while a long-term solution is sought.

An interim CTO can provide a quick but comprehensive assessment of your technology operations. They can identify areas for improvement, streamlining processes, upgrading outdated systems and optimizing technology usage to drive operational efficiency and productivity.

Implementing a new IT asset management system, automating manual processes or transitioning to a cloud-based infrastructure could be part of the transformation. These changes not only free up your team for more strategic work but also enhance your disaster recovery capabilities while reducing IT costs.

Interim CTOs, with their vast experience across various industries and companies, can introduce best practices into your organization. They can guide your team in implementing agile development methodologies, which can shorten your product development cycles and accelerate time to market.

Additionally, they can help establish a robust cybersecurity program to safeguard your data from cyber threats and lay out a comprehensive disaster recovery plan, ensuring business continuity in the event of a disaster.

Interim CTOs can craft a strategic technology roadmap that aligns perfectly with your business goals. They can help you identify key technology trends that could impact your industry in the next 5-10 years and develop a plan to adopt these technologies.

This foresight can provide a competitive edge and enable you to prioritize your technology investments effectively based on your business objectives.

Whether it’s a complex digital transformation initiative or a software development project, an interim CTO can provide expert oversight. They can manage the risks associated with these projects, coordinate the efforts of multiple teams and ensure that the project aligns with your business objectives, all while making sure the project is delivered on time and within budget.

Strategic guidance from an interim CTO can be invaluable to your executive team. They can help develop a plan to invest in new technologies that will drive business growth, keep you informed about the latest digital trends and advise you on making technology investments that align with your business strategy.

There are interim CTOs who specialize in specific technology areas, such as cloud computing, cybersecurity or data analytics. For instance, if you’re considering a cloud migration, an interim CTO with cloud computing experience can assess your needs, develop a migration plan and manage the transition. Or, if cybersecurity is a concern, an interim CTO with cybersecurity expertise can help you assess risks, implement security controls and train your employees on cybersecurity best practices.

The strategic advantage of hiring an interim CTO is evident. They can provide the expertise and guidance needed to enhance technology operations, drive strategic initiatives and position your business for success in the digital age.

Hiring the right interim CTO can be challenging, which is why engaging a third-party expert in the selection process can be a huge advantage. At BluWave, we excel in presenting tailor-made candidates who align perfectly with your specific requirements. Our deep network of pre-vetted interim CTOs, curated through rigorous evaluation, ensures that you get access to the best of the best. Even better, we can deliver these top-tier candidates within a single business day, enabling you to act quickly and confidently.

Contact our research and operations team to set up a scoping call and leverage the strategic advantages of a temporary chief technology officer.

Enterprise Resource Planning (ERP) software streamlines business processes by coordinating data flow across an organization. It provides a single source of truth and optimizes operations.

SIGN UP FOR OUR NEWSLETTER

Stay up to date with the latest PE trends, case studies on how we’re helping business builders win and more.

They are used to manage everyday business activities such as finance functions, compliance, risk management, retail, supply chain and HR.

That’s why so many PE firms seek help for their portcos in this area. Private and public companies often seek outside support, too.

Here are the primary hurdles we hear about on scoping calls where a client needs help extracting data from their ERP:

Lack of internal expertise: This is a common challenge when extracting data from enterprise resource planning (ERP) systems. Outsourcing to a third-party service provider offers access to domain experts with the knowledge and skills to efficiently extract data.

Time constraints: Outsourcing offers a faster turnaround and allows companies to focus on core business functions rather than data extraction, which can be a time-consuming process.

Complexity: Extracting data can be complex, especially if the data is spread across different modules or systems. Experienced service providers who specialize in data extraction can provide a more efficient solution and ensure that the information is accurate and reliable.

Cost: Investing in the necessary hardware and software to extract data from an ERP system can be expensive. By outsourcing the project, companies only pay for the services they need.

Need for specialized tools: Companies may not have access to the necessary specialized tools and software. These same tools will be part of a third-party service provider’s day-to-day toolkit.

Data accuracy concerns: Extracting data from an ERP system requires a high level of accuracy to ensure that the data is reliable and can be used for reporting or analysis. If you leave this to chance, you may end up making important decisions based on faulty data.

Need for customized data extraction: Companies may require customized data extraction from their ERP system, which may not be possible with existing in-house resources. Outsourcing to a third-party provider can provide customized solutions that meet the specific needs of the company.

Compliance and regulatory requirements: The data extraction may be subject to specific regulations or industry standards. Companies may not have the in-house expertise to ensure that the process meets these standards, and can benefit from the provider’s knowledge of industry-specific regulations and standards. This helps minimize the risk of regulatory violations, legal penalties and reputation damage.

Scalability: As a company grows, the amount of data generated by an ERP system may increase, and the data extraction process can become more unwieldy. There may become a point when companies don’t have the resources to handle the volume of data generated by their ERP system. Third-party providers can offer scalable solutions that can handle larger data volumes and provide ongoing support as the company grows.

If you’re ready to extract data from your ERP system, we’re here to connect you with a niche-specific, expertly vetted service provider.

We know the resource you need for your specific situation before we ever jump on a scoping call, and we’ll introduce you to two or three best-fit solutions in less than one business day.

Service Provider Type: Independent Consultant with Financial Expertise

Industry: Healthcare

The Need

Ready to sell one of its portcos, the PE firm was looking for an outside expert to provide pre-sale diligence

The PE firm was ready to sell its diagnostic supplies and equipment manufacturer and was looking for a financial expert to get them across the finish line.

The Challenge

Financial expert to help prepare a portco for sale

The individual would need to help review quality of earnings, perform a market study, validate a financial model, coach management on pitching, and most importantly, be able to close the books and handle data requests.

How we helped

Connected the client witha PE-grade CFO

BluWave provided three experienced resources – all with CFO experience – from its pre-vetted network in less than 24 hours. We were by the firm’s side throughout the vetting calls, and helped them choose a best-fit option.

The Result

Consultant comes on-site and helps the PE firm close the sale in the same calendar year

Months after signing on the independent consultant, who worked on-site throughout the process, another PE firm purchased the portco. The consultant helped the organization with pre-sale diligence, optimized its finance function and ensured a smooth handoff to new ownership.

The buyers commented on the strong foundation and high growth potential of their new asset. The selling PE firm was equally pleased with the process.

We had a great experience with the consultant. My key feedback is that he has a great temperament and worked well with us and management. He has an ability to work independently and delivered solid results.

Industry-focused firm with union experience to conduct market research, headhunt C-suite executives for portco

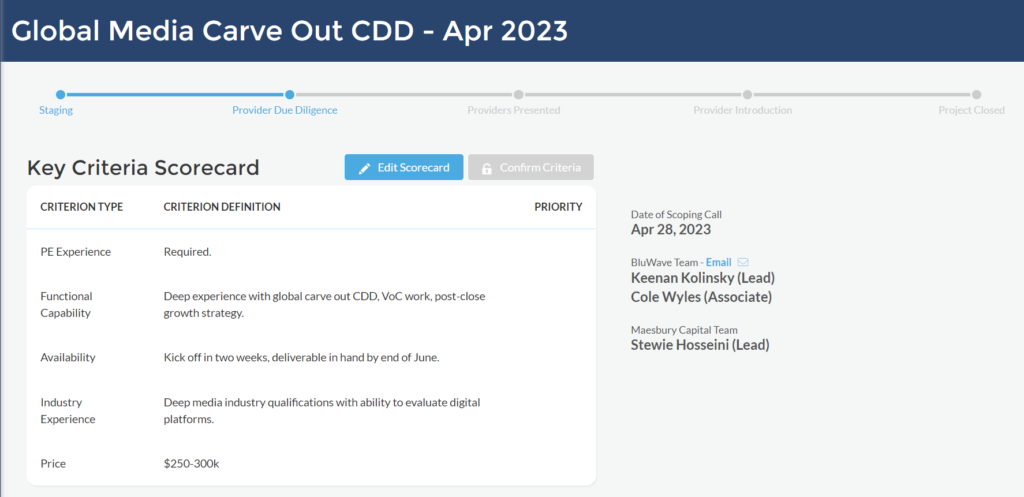

Service Area: Commercial Due Diligence: Market Study and Recruiting

Client Type: Mid-Market Private Equity Firm

Service Provider Type: PE-focused Diligence Advisory Firm

Industry: Construction and Engineering: HVAC & Plumbing

The Challenge

Prep for sale and build a corporate office team from scratch

The PE firm needed an HVAC-experienced market research firm to help with a pair of high-priority projects. With an eye on exiting soon, the firm wanted someone in the same region as their portco – the southeast U.S. – to talk to union reps, customers, facility managers, trade organization leaders and OEMs.

They were also looking to hire a CEO, CFO and Chief Labor Relations officer to build a corporate office from scratch.

How BluWave Helped

Introduced best-in-class service providers

With just a two-week timeline, we immediately presented a pair of BluWave-grade service providers with HVAC union experience. The client chose its preferred option and was introduced on a call the next business day.

The Result

Service provider sets up private equity firm for successful exit five months after introduction

The client engaged with the service provider, who completed the market study and helped them fill their executive roles. Five months later, the firm sold its portco to a large-cap PE firm after a five-year hold period.

The portco had a 400 percent revenue and EBITDA increase during the holding period, and integrated six different acquisitions in its exit year while working with a BluWave service provider.

We recommend the service provider for anything in the built environment. The team was great. Everything was great. They clearly knew the space. I’d use them again.

Whether going through an M&A, an internal crisis, a reorg or other situations that require a talent expert, here are some reasons private equity firms should consider temporary HR leaders.

Increase Efficiency and Effectiveness

A human capital leader has the opportunity to improve company operations for the short time they’ll be in their role. (Usually three to nine months.) Here are some ways they can do so.

Streamlining HR Processes

They can evaluate existing HR processes at a portfolio company, identify areas for improvement and implement changes to increase effectiveness. This may include automating repetitive tasks and standardizing processes across the organization.

For example: expediting a labor-intensive employee onboarding process with new software. They could also implement a standardized performance management system so that everyone understands how they’re evaluated.

Temporary CHROs can also collaborate with the tech team to improve data collection, storage and analysis. This makes it easier for management to make educated decisions.

One way they could do this is by creating dashboards accessible to managers. These, and other tools can streamline analysis relevant to growing the business.

Aligning HR with Business Goals

The human resources department’s objectives must also align with the portco’s goals.

Identifying and tracking KPIs – employee turnover rate, time to fill, employee engagement, DEI initiatives – is one way to do this.

The interim CHRO interview process is a great time to determine whether the person you want to hire works well across departments.

Exit interviews help managers understand why employees leave and identify what contributes to a high turnover rate. This information can be used to develop retention strategies and improve employee engagement.

Here are some of the questions an interim CHRO might ask a portco employee during an exit interview:

What made you decide to leave the company?

Is there anything you disliked about working here?

Do you have any suggestions for how we can improve?

How was your experience with your manager?

Creating Employee Retention Programs

Retention programs address the specific needs of employees, such as recognition programs, professional development and the ability to work from home, even in a hybrid situation.

Employees may also be more likely to stay if they have access to department-specific job training.

HR leaders can also use engagement surveys and focus groups to identify problems ahead of time.

Identifying Key Drivers of Employee Satisfaction

Speaking of surveys and focus groups, they not only tell HR leaders what’s going wrong but also tell them what employees like about a company. This information can help create targeted retention strategies and improve employee engagement.

Here are some of the top areas of employee satisfaction an interim chief human resources officer will want to pay attention to:

Clear communication and transparency

Opportunities for growth and development

Work-life balance

Recognition and rewards

Building a Positive Company Culture

Creating a positive company culture is no easy task, especially in the midst of a transition. That’s why it’s important to work with an interim CHRO experienced with tumultuous situations.

Besides paying attention to employee satisfaction, this person should be able to build consensus across teams.

“In a strong culture, employees feel valued,” according to Great Place To Work. “They enjoy at least some control over their jobs, instead of feeling powerless. Whether it’s by working from home, choosing their projects or trying out a new role, employees that feel valued and can make decisions achieve a higher level of performance.”

Providing Regular Feedback and Recognition

An interim CHRO can help managers to provide regular feedback and recognition to employees.

They can standardize feedback loops through surveys, one-on-one meetings, focus groups and other tactics. They should then be transparent about how they will use that information to improve the company.

It’s important to do this on a regular basis, and not as a one-off exercise.

Since this person will only be in their role for a few months, having monthly, bi-weekly or even weekly evaluations may make sense. Especially if they can develop a system that can be inherited by the person who will take on their role full-time.

An interim CHRO with experience in your industry can hit the ground running. Every business has a unique set of legal challenges, and you don’t want someone in the C-suite who has to learn on the job.

Here are some specific areas where a temporary CHRO can help with legal hurdles.

Reviewing and Updating Company Policies and Procedures

This ensures a company is compliant with all relevant laws and regulations, such as those related to labor, anti-discrimination and data privacy.

This should be done in collaboration with other executive team members as well as the legal team.

Conducting Compliance Audits

Compliance audits help identify areas of legal risk and recommend corrective actions.

The head of people can do this by developing an audit plan with a clear scope. They’ll then determine risks, gather evidence and analyze the information. In the end, they should prepare a report based on their findings.

They’ll also need to implement the plan quickly to minimize risks to the company.

Providing Training and Education

Another way to protect the company as well as equip employees is to educate them on compliance and labor laws.

Here are some resources an HR executive might use for this:

A comprehensive communication strategy informs employees about the transaction and its implications.

The head of HR may do this with a dedicated website, by holding town hall meetings or providing regular updates. They may also work with management to develop a Q&A document and establish an employee hotline.

Managing Cultural Integration

A seasoned executive will improve cross-company integration by addressing differences in culture, values and internal practices.

They do this with shared vision and values, aligning policies and procedures and promoting cross-functional collaboration.

Mary Anne Elliott, CHRO at Marsh, talked with HBR about the importance of working with other top executives on this.

“[These] meetings are a pragmatic activity. When you’re sitting with the CEO and CFO, there’s no place for academic HR,” she says. “It’s all about understanding what the organization needs to do to drive business performance and how to align those key variables.”

Assessing and Managing HR Risks

Some typical risks associated with a merger or acquisition are employee retention, legal compliance and benefits integration.

A capable temporary people leader will know how to do each of these things efficiently.

Coordinating Benefits and Compensation

Coordinating the integration of benefits and compensation packages for employees is also important.

Health insurance, retirement plans and stock options are just a few examples.

Reviewing existing benefits packages can help them identify gaps or redundancies.

Integrating HR Systems and Processes

Finally, an interim chief human resources officer can manage the integration of HR systems and processes such as payroll, performance management and employee data management.

The new, combined organization’s HR processes must be aligned with the needs of the business.

The IT department can help in this area by ensuring a smooth transition of data and systems.

Some roles are more crucial to a company’s success. The interim CHRO should identify these and devise a strategy to make sure the right talent is in place if someone leaves.

They can also identify potential leaders within the company who lack professional development.

Conducting Talent Assessments

Internal assessments help identify high performers. Since these are the people most likely to leave for another opportunity, it’s worth investing time in their development.

By aligning these evaluations with company goals and leadership needs, the employees will be better equipped for a new role.

This will open the door for them to be promoted sooner as they grow within the company.

Creating Development Programs

An interim CHRO can design development programs to help high-potential employees acquire the skills and experience needed to take on leadership roles.

These are some ways they might do that:

Rotational assignments

Mentorship programs

Professional development courses

Cross-functional team assignments

Building a Talent Pipeline

While it’s important to foster talent internally, an interim CHRO can also establish an external talent pool. Outside hires often help the company by bringing a fresh perspective to a challenging situation.

Having a group of qualified candidates on standby also saves time in the hiring process.

At BluWave, we have a highly vetted group of candidates for private equity, portco and privately owned company needs on standby. That way, we can provide you with two or three exact-fit resources within a single business day.

A comprehensive succession plan will not only focus on identifying, developing and retaining key talent, but also contingencies for unexpected departures.

Along with mentoring and coaching programs, regular performance reviews ensure that employees are ready to take on new roles when needed.

If your private equity firm or portco leader needs a human capital expert, BluWave has the world’s best temporary chief human resources officers on standby. And if you’re already in a talent role, we have tailor-made solutions to support you, too.

Everyone in our network has been rigorously evaluated while also receiving multiple recommendations from other leading PE firms.

Reach out to set up your initial scoping call with our research and operations team, and we’ll provide you with two or three exact-fit candidates, no matter how urgent your need, within one business day.

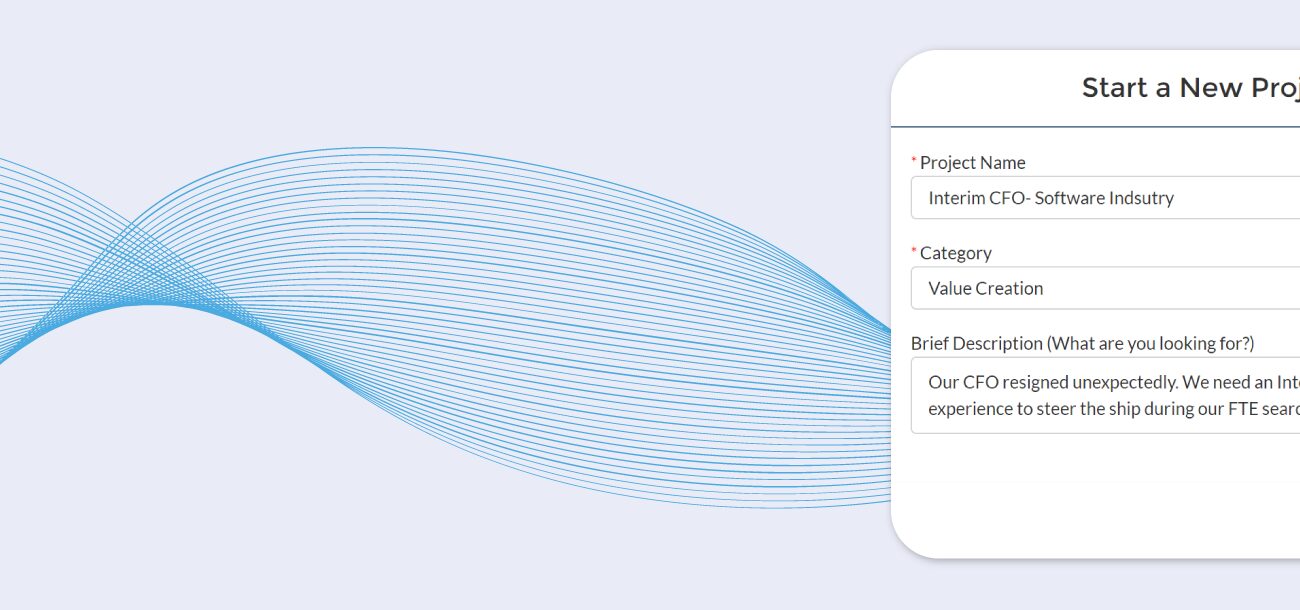

PE firm urgently needs an interim CFO to help with prep for sale

A PE managing partner came to us with a critical need for an interim CFO to lead their software portco through a sale process. Hoping to sell within the next 3 to 4 months, the managing partner was urgently looking for someone who could immediately come in to the portco, take point on gathering essential documentation for sale, manage financial projections, and serve as a leader within the portco during this transitional time. The PE firm quickly needed a PE-grade interim CFO who was available for the next 4-6 months, had deep SaaS expertise, and was able to travel onsite several days a month.

BluWave has pre-vetted providers matching client’s needs

Leveraging our founder’s 20 years in private equity, we have extensive frameworks for assessing PE-grade prep for sale needs. BluWave utilizes technology, data, and human ingenuity to pre-map, assess, monitor, and maintain deep pools of interim CFOs that uniquely meet the private equity standard. We interviewed the PE firm to understand their specific key criteria, and then connected the client with the select pre-vetted interim CFOs from our invitation-only Intelligent Network that fit their exacting needs.

Firm engages interim CFO and begins prep for sale

The day after the initial scoping call, the PE firm and portfolio company were introduced to two PE-grade interim CFO that specialized in helping software companies prepare for sale. The client selected their ideal choice. The firm engaged the interim executive and was able to confidently proceed with their prep for sale process thanks to the leadership of the CFO we connected them with.

PE firm urgently needs leadership coach for prep for sale process

A PE vice president came to us with a critical need for leadership coaching services to build up one of their portco’s mid-level management teams in preparation for sale. Looking to exit the company within the next year and with several high performing mid-level leaders with little to no executive experience, they were in critical need of a provider that could coach this cohort up for the sale process. The firm specifically wanted a provider that had experience in a PE setting, practice around exit prep, and expertise in coaching the management level just under the C-suite.

Leveraging our founder’s 20 years in private equity, we have extensive frameworks for assessing PE-grade prep for sale needs. BluWave utilizes technology, data, and human ingenuity to pre-map, assess, monitor, and maintain deep pools of leadership coaching consultants that uniquely meet the private equity standard. We interviewed the PE firm to understand their specific key criteria, and then connected the client with the select pre-vetted executive coaches from our invitation-only Intelligent Network that fit their exacting needs.

Firm engages provider to coach management through prep for sale process

Within less than 24 hours from the initial scoping call, the PE firm was introduced to an exact-fit leadership coaching provider. The client engaged the recommended provider and was able to confidently move forward in their efforts to sell the business knowing that their management team would now have the proper coaching required to successfully deliver on their roadshow presentations.

As part of an ongoing series, we’re sharing real-time trending topics we are hearing from the hundreds of PE firms we work with. In our most recent installment, Erez Schnaittacher, BluWave vice president of client coverage, shares the importance of interim CFOs and why they are a vital resource all PE firms should be taking advantage of. Learn more by watching the video below.

Interested in connecting with interim CFOs? Contact us here to quickly get connected to the exact-fit interim CFO you need.

The CFO role is one of the most critical seats in a business. The position plays a key role in ensuring that a business is strong and if PE-backed, that the investment is successful. Because this seat is vital to a company’s success, it is important that it is not left open, and is also filled by someone who possesses the right skillset to execute on the demands that come with being a CFO.

To ensure that both of these are always the case, PE firms often turn towards interim CFOs. At BluWave, we equip our private equity firm clients with interim CFOs for various due diligence, value creation, and prep-for-sale needs. Here are some of the most common use cases for bringing in interim CFOs:

Number one, unanticipated departures. When CFOs unexpectedly resign, it can leave a company’s finance function in chaos. We help PE firms combat this by providing them with exact-fit interim CFOs who can quickly step in, fill the shoes of the role, and keep the ship steady while the search for a permanent placement kicks off.

Number two, longer than normal hiring processes. Even when a CFO seat is expected to be vacant within a certain timeframe, sourcing a candidate to step in at the exact time you need them to can be challenging. With hiring processes taking longer than normal, interim CFOs can help bridge the gap, giving you extra time to ensure you hire the best-fit person for the job.

Number three, professionalizing new portcos’ finance functions. We are supporting many PE firms as soon as a deal closes, by supplying them with interim CFOs. These firms are bringing in these individuals to help new portcos’ finance functions understand what it means to be PE-grade, and help them get the right monthly performance packages in place to ensure that the PE firm is getting the info it needs.

And finally, number four, prep for sale processes. Our clients bring in interim CFOs to respond to diligence requests, assess data, and pull reports prior to a sale. By bringing in an extra set of hands to take care of the extra workload that comes with a sale process, FTEs are freed up to maintain focus on keeping the daily routines going, without causing a delay on the sale process. The modern-day M&A process is fast and furious, valuations decline the second you have to hit the pause button, making it crucial to keep the momentum.

Interim CFOs are one of the most versatile and useful resources available to private equity firms. Hundreds of leading firms come to us with their interim CFOs because of our ability to know before they need, hone in on individuals that meet their specific, unique criteria, and quickly connect them to the select few that are exact-fit.

If we can support your interim CFO needs, please contact us at insights@bluwave.net.

I get asked a lot of questions about how to build a business, and how to do it with as few headaches as possible. Not that I’ve totally figured it out, but I’ve certainly made my fair share of missteps and gratefully have learned something along the way. From investing, to hiring, to reducing headcount, to managing the ups and downs of an economic recovery period—one thing remains unchanged: leadership matters. And if you’re talking about key leadership positions, the one that companies most often get wrong is the CFO.

Why? Well, the answers are as varied as the reasons they fail, but it generally has to do with asking the right questions from the beginning. In other words, the interview process is often to blame.

I wrote an article for CFO Magazine about “hiring the right interim CFO” and how to ensure you set your company up for success when it comes to hiring one of the most important positions. Whether you are looking for an interim CFO (who can move into a full-time position) or looking for a full-time financial executive, here are some things you should know before you greenlight your new hire:

8 Things To Know Before Hiring An Interim CFO

If you are a PE-owned company and need to bring in a short-term finance chief, find someone who has worked for a PE-backed company before.

The interim executive needs to have a track record of wins. That generally means a significant tenure at multiple companies.

Find someone with industry experience, because it’s much easier to stand at the finance helm of a manufacturing, healthcare, IT, or services company if you’ve done it before.

Similarly, the interim CFO should have experience working for a company of similar size and scale.

It’s not enough to understand the numbers (sales, revenue, overhead) — you need someone who understands what the numbers mean.

For the best results, find a pro who has a high IQ and a high EQ (emotional intelligence), because the interim CFO needs to quickly gain favor from others in the organization to gather information and build a story around the numbers.

Be sure to have conversations with key stakeholders in a candidate’s prior roles. Choose the references; do not use the references the candidate gives.

While enthusiasm is a wonderful aspect of a new leader, a short-term executive should have a stabilizing effect, not a disruptive one.

For more details and to read the full article in CFO Magazine, click here.