Recently, BluWave founder & CEO, Sean Mooney, spoke with Brian C. Adams, founder of Excelsior Capital, on The Capital Club podcast. On the podcast, their conversation covered the private equity industry and how there is currently a struggle to find quality assets, how PE is embracing technology to address labor shortages, and COVID’s impact on the industry.

Interested in listening to this episode of The Capital Club? Click below.

Gain more insights from Sean on PE by listening to our very own Karma School of Business podcast.

You can also glean more wisdom from Sean through other podcasts he has been a guest on, including:

If we can help you be successful by quickly connecting you to the PE-grade, pre-vetted, third parties you need, give us a shout.

Podcast Transcript:

Brian Adams: [00:00:30] Hello and welcome to the Excelsior Capital Club podcast. I have with me today Sean Mooney. Sean is the founder and CEO of BluWave, an Intelligent Marketplace trusted by more than 500 of the world’s top private equity firms, leading family offices, and thousands of proactive businesses to connect them with best-in-class third-party resources they need for due diligence, value creation, and preparing for sale.

Sean founded BluWave as a solution [00:01:00] to a problem he faced every day while in the private equity industry for nearly 20 years. Sean, thanks for joining us.

Sean Mooney: Brian, it’s great to be here with you.

BA: Good to see you, man. And if we act casual on the show, it’s because Sean and I know each other socially. We both live in Nashville, our kids go to school together, and we bump into each other at a lot of events. And I’ve been thinking about having him on for a while, so I’m glad we could finally do it.

And you were maybe an early wave of a lot of these [00:01:30] private equity folks moving from New York and elsewhere to Nashville. Before we get into kind of the core of the business, I’d love to hear your commentary on what led you to that choice to move to town, and how that experience has been, and what you’re seeing especially within the asset management, ALTS, private equity, family office world of this influx of capital and personnel into the middle-Tennessee region.

SM: Absolutely. So I moved to Nashville almost six years ago, which now makes me almost [00:02:00] as local as anyone, I expect. And now my big fear is all the people like me moving here can totally ruin this place. So we want to be the last ones in, but Nashville has been everything we ever hoped it could be.

The people are amazing, the food is great. It’s albeit a heavier dining experience, which caused me to probably put on some weight I had to lose eventually.

But we moved here really to start a business and to seek, in some ways, a better life, or at least an easier [00:02:30] one, even though we came from a place that we really loved. We were living in Darien, Connecticut. And my wife grew up in Connecticut, and we absolutely, I think, appreciated where we came from but thought there’s maybe a way to change the dynamic.

And then really as a result of wanting to start a company and be an entrepreneur, we had this idea that it would be pretty expensive to start a business in New York. And so I did a market study, and that’s why we’re here. I looked at columns on a spreadsheet, one of which said “fun,” [00:03:00] and I think my wife said, “You’re taking all the fun out of this, can we do it some other way?” But it worked.

BA: And it’s been just tremendous to see it. I’ve been here 15 years. My wife’s a local native, and it’s wild. And I don’t think it’s going to change anytime soon. So yeah, you’re definitely old school. Six years qualifies as an OG these days.

Let’s get into the business and your journey there by starting with this question, because, not to age you, but you’ve been in private equity for a while now. Is [00:03:30] private equity taking over the world?

SM: It’s a very good question. I don’t know that it’s taking over the world, but it’s certainly representative of the economy and a major force in the economy. There are, depending how you calculate it, 5,000 private equity funds in the US alone. There are hundreds of billions of dollars of dry capital. They’re investing across the economy, and it’s moved from, and maybe evolved from, an industry that was in some ways, [00:04:00] in the early days, as much about arbitrage, where you could invest in an asset in maybe a way that was less efficient. You could optimize the company and then sell it more efficiently through an investment banker process. The industry, like anything where there’s great opportunity, has matured quite substantially, which means they’re buying it and investing it at the intersection much closer to supply and demand.

Which means in terms of its impact on the world, [00:04:30] whether it’s altruistic or selfishly altruistic, they’re now transforming companies, in some ways because they have to. And so they’re fundamentally making these businesses bigger, better, more people, more innovation, because the economics of the industry and econ 101 is compelling them to do so.

So it’s in every pocket of the industry, and I think they’re having a pretty meaningful impact on the US economy, but also global economy, in terms of growth and development.

BA: Do you think it’s positive [00:05:00] there are so fewer publicly traded companies, or companies are waiting longer to go public? I know I’ve heard criticism on both sides of the dial that private equity is a very powerful force for job creation, value creation, that a lot of these companies that were public were zombies or living on debt and weren’t actually creating value for stakeholders or shareholders.

What’s your review there on what is certainly something we’ve seen [00:05:30] play out pretty dramatically over the last five or 10 years?

SM: Yeah, I think the private equity industry evolved really because of the in-between for companies that were smaller than those who could go public. And you go back to the roots of the industry, your options as a business builder and owner was to borrow bank debt. If you happened to be on the West Coast, you could get venture capital, or if you got big enough you could go public, or you could sell your entire company to another company.

[00:06:00] And the early developers and builders of the industry realized there had to be a middle market where smaller to middle-market, or medium, to even big-size companies could access capitals in the way that weren’t available at public companies.

I think where private equity has an advantage is they can think further out. One of the trappings, as you talk with people who run public companies, is that they fall victim to this quarterly cadence, where they have to make someone happy every single quarter. [00:06:30] And so their decisions become quite tactical, because that’s where the incentives are.

The private equity businesses I think in some ways are liberated from that, because they can think three to 10 years ahead and make decisions that are probably more chess-like than checkers-like.

BA: So as you referenced, private equity has matured dramatically and continues to. I think your company is evidence of that, in terms of you’re an advisory consulting firm for this [00:07:00] niche industry, so you’re like a niche consultant for a niche industry, which is just how deep this ecosystem goes.

I want to tie in the family office world. I’ve had a lot of conversations with folks in that space that say that family offices are a superior investment solution to even private equity. You said private equity, long-term hold, not beholden to quarter-to-quarter reporting numbers, but families seem to be able to take [00:07:30] it to that next step where they have a 50-, maybe 100-year time horizon, super flexible capital.

Are you seeing family offices behave more like private equity funds and private equity funds behaving more like family offices? There almost seems to be a crossing of the streams in that regard.

SM: I think you’re absolutely right, and if you look at some of the criticism of private equity and in the world as they say, “Well, they’re horizon maybe is too short. They’re looking for three-year [00:08:00] periods. Why aren’t they looking to build seven, eight, nine, 10 years?”

And then the family offices will say, “Hey, we have 100-year perspectives. We have a multi-generational perspective,” but maybe they can’t bring the same resources to bear that a mechanized private equity fund can. And I think it’s a very great observation that you had, that they’re kind of starting to meet in the middle, where private equity firms are starting to have longer time horizons, and family offices are starting to want to make direct investments themselves.

[00:08:30] And in some ways businesses like BluWave evolved to serve both those needs. When I was in private equity for almost 20 years, we had to transform these companies. We had to use third parties. Third parties were really hard to use, because every need was different. And I had nowhere to go other than having very expensive, highly educated people Google “problem in industry” and call buddies, and that’s how we found the resources we would use. I said, “Why isn’t there like a [00:09:00] Yelp or an Amazon for business?” And that’s what we created. So it’s this magic toolbox for business builders, where they can go to one place to get the very best for everything they need.

In the same vein, family offices are using us because they want to be able to make direct investments, and they don’t have the mechanized teams that private equity can. So they come to us and say, “What are the groups that I can use to very effectively assess a company in diligence, [00:09:30] but then also build the company with a long horizon period of time, where maybe slower but steadier wins the race? And maybe it’s not the fastest way to run, but it’s the most certain path to build this company to something transformational.”

And so both of these groups are also coming to us for the same resources but for, in some ways, different reasons.

BA: And have you seen, now that the wealth creation has been so immense, call it the last five [00:10:00] or 10 years, especially within the tech world. Some of these family offices seem to be behaving like just typical private equity firms in many ways. They have an internal deal team, they have a CIO, they have a CEO, whole full C-suite built out including Tech Stack. And what I’ve been hearing more and more of is that they are competing directly with, not only the old wirehouses, but the larger private equity firms and venture capital firms, for deals and talent.

Could [00:10:30] you maybe provide some commentary on what you’re hearing and seeing from your clients to that regard?

SM: 100%. So there are a number of family offices that have kind of mechanized their capabilities, particularly the families where they have knowhow from the businesses that they’ve built, whether they currently have an operating company or they did have an operating company, and you had a family office, patriarch, matriarch, who really had a lifetime of building businesses. So there’s a lot of knowhow [00:11:00] within these companies.

And so they’re building out teams to do that. And I think they also in some ways view the world through the word “and” versus “or”. So it’s not like they’re not also investing in GPs, because they’re still doing that. And they’re also co-investing with GPs, which is a great way to get started in direct investing, by the way, is co-invest with the GPs where you already have relationships, where you can get that direct investment and see maybe a little bit how the process works.

But they’re also building their own [00:11:30] teams, and they’re doing it through a comprehensive asset-allocation model where they can do kind of A, B and C versus A or B or C.

BA: So along those lines, in terms of your firm and how you work, you have a multifaceted business, but when it comes to the deals, say M&A, direct investing, who are the groups that are getting it right and why? And then obviously the flip side, what [00:12:00] are the potholes that people keep stepping into that don’t allow them to successfully invest directly into this M&A space?

SM: It’s really interesting from the vantage of BluWave, because we work with more than 500 of the top private equity funds across the country. And I kind of joke with my friends who are still in PE, I was pretty good at what I did when I was in PE. I was a partner at a really top-notch fund in New York.

There were certainly others who were [00:12:30] better than me, but I was pretty good. And I kind of joke to them, after seeing over years and years how 500 PE firms do things, I’d be almost like Neo if I ever came back to PE, where I’d see the ones and zeros cascading down, seeing the world in slow motion.

But there is a pattern to what we see in terms of really top-notch PE firms. And one of the things that we do as part of our firm is we have this Karma School of Business, where we just try to do good things with good people. [00:13:00] And we started having LPs coming to us saying, whether it’s family officers or institutional investors saying, “What do you see? What are the patterns of really good firms that we should look for?”

And we thought, “Why don’t we just put it out there and say, ‘Here’s what we look for,'” and then recognize those who we think do it really well? And so we came up with a list of top PE innovators, a group of 50 firms that all do it really well.

And we really look for four things, or things that we kind of notice that are [00:13:30] differential and innovative in PE. One, it’s the PE firms that recognize that the business of PE has to be run like a business and less like a partnership.

And so they’re treating their business as if there’s a front end, there’s a back end, there’s operations, there’s marketing, there’s sales, everything that they would’ve run one of their own portfolio companies with. And there are companies that are starting to do that really well within private equity.

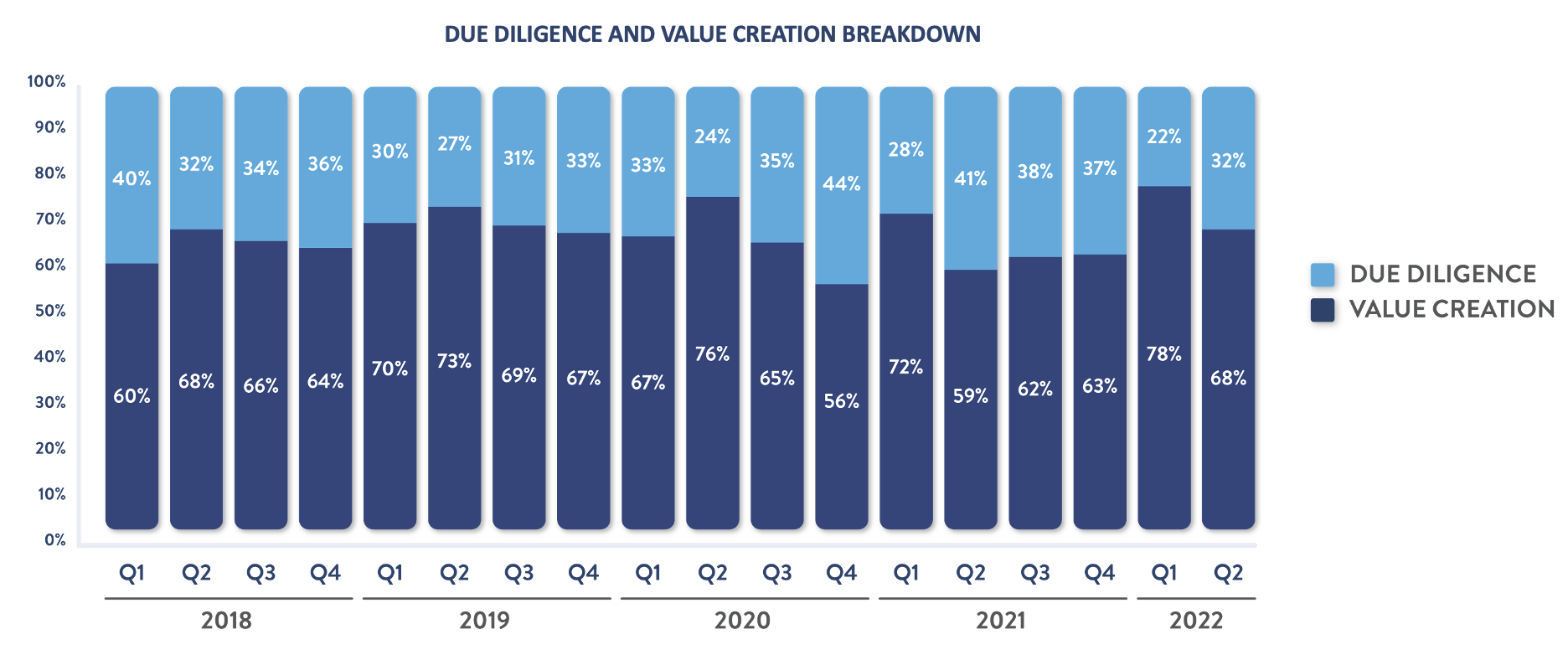

Two, they look at due diligence with an eye towards [00:14:00] transformation in equipping value-creation plans. And so when I started in PE, so much of the world was about trust and verify. Are the seller’s representations correct with what the business actually is? Check the numbers, make sure they’re paying for their Microsoft licenses, maybe there’s air conditioning in the server closet.

Now, it’s how do we fundamentally change this company, turn it into something that it was never intended to be, because we’re paying a nearly perfect price [00:14:30] for an imperfect business? Where it was exactly opposite when I was coming up in PE. And so they’re starting with the fact that they’re going to fundamentally make a bigger and better, more valuable business.

And then next, we look at companies that really are proactive in value creation. And they’re saying, “We’re going to not only find things out, but do something about it in partnership with the leadership teams in our portfolio companies.”

And then lastly, the thing that we think is really important is the concept of ESG. It’s this idea that you can have broccoli [00:15:00] with cheese on it; you can do good things for the business that also align with things that are good for the world, and they don’t have to be mutually exclusive.

And so there are businesses, a lot of the PE firms are doing a lot of these great things. And in some ways they’re just not getting credit for it, because they didn’t know that they could categorize the stuff that they’re already doing, falls within this concept called ESG, which is getting more and more clarity as time goes on.

So I don’t know if that addresses it, but that’s kind of how we looked at it internally, at least have recognized those who do it well.

BA: [00:15:30] And in terms of these red flags, things that maybe when you put your consultant advisory hat on, if somebody listening is considering investing with a group or evaluating a direct co-investment opportunity, what are some warning signs that you see that over and over again lead to poor results?

SM: Yeah, it’s a really good question. And part of the challenge is that the cliche in private equity [00:16:00] is you’ve seen one private equity fund, you’ve see one private equity fund. And so I think rather than saying red flags, I would look for groups that do those four things, and they treat their business like a business. They know that you have to be hands on in both diligence and value creation, and then you’re tracking the things you’re doing that are holistically improving companies.

If they’re not doing those four things, that would almost be my red flag. If they’re not meeting those standards or if they’re not making steps towards doing [00:16:30] that, then I would probably want to dig deeper.

BA: You referenced a big number in terms of the number of private equity funds active today and the capital behind them. I’ve always wondered, I mean I go to these networking events, and I have a lot of friends who are GP sponsors. How can the ecosystem support as many lower-middle-market buyout firms as there are in the world? And how do multiples in valuations [00:17:00] sustain that investment thesis?

SM: Another great question. In some ways econ 101 is playing out of the industry. And what’s kind of telling is the business… this is kind of anecdotal. When I started in the industry in the late ’90s, early 2000s in PE, our base case models would start in the thirties, in terms of 30% IRRs.

And then when I spun out to pursue this entrepreneurial dream here, my models were [00:17:30] in the low twenties, high teens. And in some ways you say, “Wow, that’s a lot of efficiency that’s become part of the ecosystem as the industry’s matured.” And every industry matures over time.

And it’s easy for me to say that’s a huge decline and everything’s relative. But at the end of the day, the industry is still pretty much beating every benchmark. And so for me, when I came in, I remember I was like, “Wow, I wish I was 10 years older.” It was [00:18:00] like when you’re a junior in the industry and the economics don’t really fall to you. And then every 10 years I would say, “I wish I were 10 years older.” And I think what I came to appreciate is it’s still really good, it’s just not what it used to be.

And so it’s kind of like traffic in Nashville. For those who moved here from New York, where it was rush day, I-95 was always packed. Whereas when I moved to Nashville with I-65, it’s really still a rush hour. And so both are still, the rush hour is still [00:18:30] pretty good, it’s just not what it used to be.

And so I think there’s still plenty of interesting economics in the industry. It’s just not what it used to be. But then again, it’s also a lot more accessible to a broader pool of investors, whereas in the early days, it was really a pretty small ecosystem that was not only exclusive to being in the industry, but also to those who could invest in it. So I guess it’s two sides of the coin.

BA: So we’re recording this heading into the second half of the year 2022. What are the investing themes that you see going on internally with GPs right now, and then what is exciting LPs [00:19:30] in terms of opportunity, thesis, et cetera?

SM: Obviously the big thing that is on everyone’s mind right now is this kind of triple play of economic pressures associated with Asia, Ukraine, inflation, and Federal Reserve policy trying to land playing and taking inflation down, after being at historic highs. And so the industry is, first and foremost, I think, getting [00:20:00] selective.

The PE world understands that they need to invest throughout economic cycles, and I think they’re very good at that, but they are looking at quality assets, and so the quality assets are still absolutely trading and active. PE firms themselves though, they’re saying, “We’re going to be more selective and maybe not lean as far out on our skis as we would’ve three years ago, because the opportunity to de-lever in between and professionalize, the runway’s just a little shorter.”

The one [00:20:30] thing that I think the PE industry is really good at, though, and we’ll be presenting data in the not-too-near future that kind of demonstrates this, is they’re really good at running towards the storm versus running away. And so when they see economic challenges, they view it as an opportunity by being able to use what they’re really good at. They’re able to quickly grab information, assimilate it, make decisions, and then act on it, [00:21:00] and use that to their advantage. While others maybe kind of circle wagons and maybe cower in the face of the storm, they run towards it.

So a lot of the PE firms that we talk with are saying, “This is a time for opportunity, where we can maybe invest at better multiples. Maybe we can consolidate market segments where competitors will be available. We can bring talent in that historically was never available and suddenly they are because people [00:21:30] are letting people go. We can grab and expand in segments and bring in other products while people are maybe retracting.”

And I think all of this comes from that longer perspective, but also the agility and the proactiveness of the industry. And so I think that’s one of the reasons why you see the big institutional money liking it, because they’re really good at generating returns through the peaks and troughs.

BA: Let’s talk about human talent, human capital. That’s part of your business is finding the right professionals [00:22:00] for the right groups. How fierce is that competition right now, and have you seen compensation packages? Where are they relative to the last 20 years of your experience?

SM: Yeah, it’s everywhere. It’s funny. Well, not funny. It’s interesting. We have forums where we’ll bring cohorts of PE together, and we just had one. And almost every one we do, the topic is human capital.

And one of the main topics of the day that we were all discussing was [00:22:30] one of the biggest inflationary pressures in the entire economy right now is labor wages. And that doesn’t get nearly the credit that oil and other kind of commodities do.

Labor wages have gone up substantially, in part because there’s scarcity of labor, but all the costs that every day all of us are experiencing, our team members and employees have to bear that too. So the companies have to pass those on so our own employees can kind of keep up.

And so [00:23:00] that’s something that I think where you have a combination of people who have left the labor force, so there’s fewer people in it, you have inflationary pressures that are going all the way down to inflation, it’s hard to push labor wages onto customers, if you will.

So the pressure is everywhere, and it’s certainly going all the way to even the private equity professionals, investment banking professionals, attorneys. Everyone is feeling it right now, just like I think any other industry is. And they’re doing what they [00:23:30] can to communicate things like total rewards, like all the other good things that come with being in a great company.

And the other thing that’s been really kind of fascinating to watch within private equity is this concept of culture. When I came up, I’ll profess, it wasn’t something that people really focused on. It was a bunch of type-A-plus people who took hills, and they would take that hill every time they needed to, but they didn’t think about the work experience.

So in some ways it’s been a positive on the industry, because the industry’s really [00:24:00] leaning in and appreciating things like corporate values and cultures, even within the firms themselves. And that’s another way they’re addressing it, which net-net, I think is going to be a catalyst for really good. And not only that industry but throughout the economy.

BA: One of the things I wanted to talk to you about was this generational shift happening amongst GPs. I like how you talked about how the best-in-class private equity groups treat their companies like the businesses they own and less like an old-school partnership.

I won’t name names, but I’ve seen and experienced [00:24:30] some divorces and blowups happening in Nashville, because they cannot manage through this transition of first-generation GP to a second-generation GP. And I would assume it’s only going to accelerate as these Baby Boomers get older and try to figure out what to do.

What are you seeing in terms of that dynamic playing out amongst your clients? How are people addressing it? Is it creating opportunity? Is it a risk that LPs need to be aware of, et cetera?

SM: [00:25:00] It’s another very timely topic in private equity. And if you ask why are there 5,000 private equity firms, in part, the point that you’re talking about, Ryan, is one of the primary reasons. The firms that started in the industry G1 or G1.5 of PE, they didn’t have these continuity plans in place.

And so ultimately, you would get this kind of tectonic pressure between junior partners and the founding partners. And [00:25:30] what would happen eventually is the junior partners would get fed up and they’d found a fund, and they’d bring out their own fund. And then they’d start their own fund and they don’t do the same thing. And then there’s the junior and senior partner tectonic pressure, and then their junior partners spin out.

And so this has been the circle of life and private equity for a long time. And I think what’s happening, everyone’s seen this movie enough times now that we’re really starting to see a lot of the GPs being thoughtful about this. And it’s really [00:26:00] kind of these next-gen PE firms that have maybe seen it happen a couple of times, where they’re putting transition continuity plans in place.

The other things that are happening is you have some of these funds that are able to come in that are almost like secondary funds and take positions in GPs that facilitate those transitions.

And so they’re taking some of the economic pressure off of the founders to let them kind of monetize this franchise that they’ve built and want to be rewarded for that, while also allowing [00:26:30] new junior partners to come up. So it’s a very important topic. It’s something that I think the industry is getting better at, but still needs to make progress on as they realize that they’re in the business of a business, and not the business of a partnership, particularly if they want continuity and a sustaining legacy of a firm.

BA: You were really good during COVID about being communicative, transparent. You have a great newsletter that I want to call out at the end of the show as well. And [00:27:00] you were really good about being engaged during COVID. I read all your stuff; it was terrific.

Now with the benefit of hindsight, what were some of the things that forced the industry to improve because of COVID? And what are some of the negative implications of that two-year span, hopefully, that you’ve seen remain in the industry?

SM: Yeah, it’s a complicated question. There’s a lot of things that came out of, like anything [00:27:30] in crisis, that end up being very positive. I think that the single biggest shift that we saw take place is this kind of embracement of the complexity of humanity. As labor shortages were driven and everyone was kind of broken apart into these little square boxes on Zoom, people had to figure things out. They had to figure out things like culture. They had to figure out things like how to keep people engaged.

So if we [00:28:00] look at this kind of engine at BluWave, in the beginning of 2018, 17% of the projects that came through the BluWave marketplace were related to human capital And in the first quarter of 2022, 42% of the projects were. And so the private equity industry, I think, is very much investing in it.

And so the hottest hire in all of private equity is head of human capital. And so they’re realizing that you have to holistically manage the people side and bring this kind of humanity to an industry [00:28:30] that’s been kind of a dollars-and-cents industry. And not because they meant to be unfocused on it; there were just other things that were kind of gaining mindshare. And so I think that’s one of the biggest things.

The other thing: I think it really calmed their ability to manage through a crisis. And so, one of the things I alluded to earlier is what we saw in our data. We see very interesting data that comes through these projects that you can discern trends through. I think they learn [00:29:00] to be incredibly even more agile in bringing methodologies of dealing with tough times and managing through them. And so I think that’s something that’s also been very positive.

As you think about super trends, crises in some ways catalyze these things that never quite got going but were always kind of bubbling up.

And so two super trends that I think PE has really gotten behind that were always, like everyone said was the next thing, always has been, always will be, is, one, digitization. [00:29:30] And so we’re really seeing groups jump in and realize that you don’t need to have people typing stuff in. You can digitize things, you can automate things, you can let the robots do the stuff that robots are good at and have the people do the things that people like doing.

So we saw a lot of embracement about technology that not only becomes more efficient, but I think it improves satisfaction within the team members, because they get to do the things that they like doing, that humans like doing.

The other thing that’s really catalyzed I think in this, is the whole concept of analytics. It really [00:30:00] caused the really good firms to dive into their data to help make decisions, and realize that if you have good data, you can make better decisions. And if you rapidly iterate around it, you can make very interesting decisions about business and life, et cetera.

And so those were some of the things that really, I think, catalyzed, and the super trends that became trends not only in PE, but elsewhere.

And so I’ll pause there. I don’t know if that kind of addresses it, and we can do the flip side of the coin as well.

BA: Yeah, no, I think [00:30:30] seeing the same thing play out in my industry in terms of real estate, pretty-old school traditional business. And COVID taught all of us that we can do much more digitally, we can do much more automated, and you realize that you can spend your time more strategically for highest and best use of the enterprise.

So let’s go to the other side. I mean, what are some things that maybe you’ve seen change because of COVID that are negative for the industry, or you’re [00:31:00] not especially excited about?

SM: I think the biggest challenge that everyone is working through is how do you learn how to operate in this hybrid world that has evolved. Particularly industries like private equity, investment banking, legal professions, they very much have apprenticeship models, where you need lots and lots and lots of laps around the track to learn things, and there’s a pattern recognition.

I think a lot of the industry is struggling [00:31:30] to equip the more up-and-coming professionals with that apprenticeship, and they’ve kind of lost out. And the hard thing that I think everyone’s dealing with is what’s that right middle ground. Because in some ways, there’s a lot that’s come out of that’s great about this hybrid model, where you don’t have to be maybe cutting out a lot of face time.

On the flip side, people I think are having a lot of mental health issues, because when you work at home, you live at work. And so finding that [00:32:00] right balance is something that I think everyone in PE is struggling with. But I think probably everywhere in the world is right now.

And so the big transition that will be very interesting to see how it takes place is where that kind of shakes out. I think you’re also seeing a lot of firms realize that, I think too often people view the world through binary lenses. You’re either going to be fully virtual or fully in person. It’s that [00:32:30] in-between that’s going to make the difference.

And I think a lot of firms that have at least have found that balance are getting a real competitive advantage, because they’re getting people collaborating, seeing people, and able to find that instant feedback loop a little more beneficial while also getting the benefits of some of the hybrid models.

BA: Many of the larger financial services folks globally have proclaimed that globalization has peaked, and now we’re [00:33:00] in an era of deglobalization. When you talk to private equity groups, GPs and sponsors and big LPs, are they seeing that, feeling it? Do you believe that?

SM: Yeah, I think where I would characterize it is the pendulum is, once again, it’s not going to be globalization or not. I think like everything, we always see the pendulum swings way too far one way, and then goes the other.

What COVID has catalyzed [00:33:30] in so many people of mind is supply chain dependency. And particularly when you’re dependent on another country’s kind of posture as it relates to open or closed, and you have to get things eight weeks on the water, and then you can’t get them through the port, people have really appreciated that you can’t have an n=1 supply chain, because then you get these huge systematic shifts that come in and you’re left with nothing to provide, because the just-in-time nature of all these supply [00:34:00] chains has kind of exposed these really, really dramatic weaknesses in this global ecosystem that we’ve built.

And so I think what you’re seeing is a lot of people saying we have to have more of a portfolio approach. We can’t just leave China. China is one of the world’s growing fastest growing markets, and has been and will be increasingly important, but you can’t have everything over there.

You can’t, in the same vein, you can’t have everything here. It’s this idea of maybe spreading [00:34:30] your chips a little bit and playing more of a risk-adjusted game than being wholly dependent on things.

BA: You put out, I’ve referenced this before, a terrific newsletter, and one of my favorite parts is the comfort food is good, but the life hacks are great. You have any favorites yourselves, or did you get outside feedback on a few versus the others?

SM: It’s so funny. On these newsletters, the single biggest thing that gets engaged with is the life hacks.

BA: Totally. Yeah, it’s great.

SM: So during [00:35:00] COVID, one of my big accomplishments that I was proud about was that apparently I sold out the entire country of inflatable movie screens for your backyard. In all these life hacks there’s no economic interest in it. It’s just things that I think are cool and interesting, and I’ve always been a curious person. And to be very clear, I don’t make any money on these things, it’s just things that I like.

And so the inflatable movie screen was a really popular one in the summer of 2020. This [00:35:30] year, people are traveling again right now. I found this little gizmo that clicks onto the tray of the plane in front of you, where you can hold your iPhone and watch a TV show. It’s like 12 or 13 bucks on Amazon. It’s great. Every time I’m on a plane, some people ask me what that is.

BA: I love it.

SM: I guess with the two things with summer coming is my tips. One is for steaks. For those of you who like steaks, there’s a concept called the reverse sear. [00:36:00] And so if you Google that on the Internet, it’ll show you this amazing way to cook a perfectly, whatever temperature steak you like. Medium rare is what I prefer.

And so what you do is you slowly cook it at low temperatures on your, I use a Big Green Egg. And if you do that, you take it up to temperature very slowly, and then you sear it at the very end to get that caramelization from the Maillard effect that people really like. And so if you really want an amazing steak this summer, look up the reverse [00:36:30] sear.

And then the other thing that I’ve added to my game, care of my wife, is this little Breville smoke gun, and you can put these little smoke tips in them, and you can kind of add a smoke essence to any food, but you can also put them in a summer cocktail and make it taste a little smoky. And it’s just a cool gizmo, and it adds some theater to whatever you’re making if you have people over and you can show them, fire up this gizmo, and it’s really kind of a lot of fun.

BA: Love it. Love it. And [00:37:00] I own a Traeger, and the reverse sear, it’s like the amateur Green Egg, but-

SM: The Traegers are legit.

BA: But it works. It works. It does work.

Sean, I want to thank you for the time. It’s been awesome. Like I said, definitely want people to check out the newsletter, the site. If you’re at all involved with private equity, you need to connect with Sean’s firm, because they know everybody, and they’re doing incredibly good work.

If people are interested engaging with you and the firm, what’s the best way for them to get in touch?

SM: So you can find us [00:37:30] on the Internet at BluWave.net. You can also find me on LinkedIn. We’re incredibly responsive. Anytime you need us, we’re here to help. And if you’re from Darien, Connecticut, you might recognize the name of our company.

BA: As a lacrosse player, I knew it right away. I definitely recognized it. So BluWave, I love it.

Sean, thank you so much for the time. This is great, and I wish you the best [00:38:00] of luck. I hope you have an awesome summer, and I’m sure I’ll bump into you in town, soon.

SM: Brian, thanks so much. I look forward to catching up with you sooner than later.